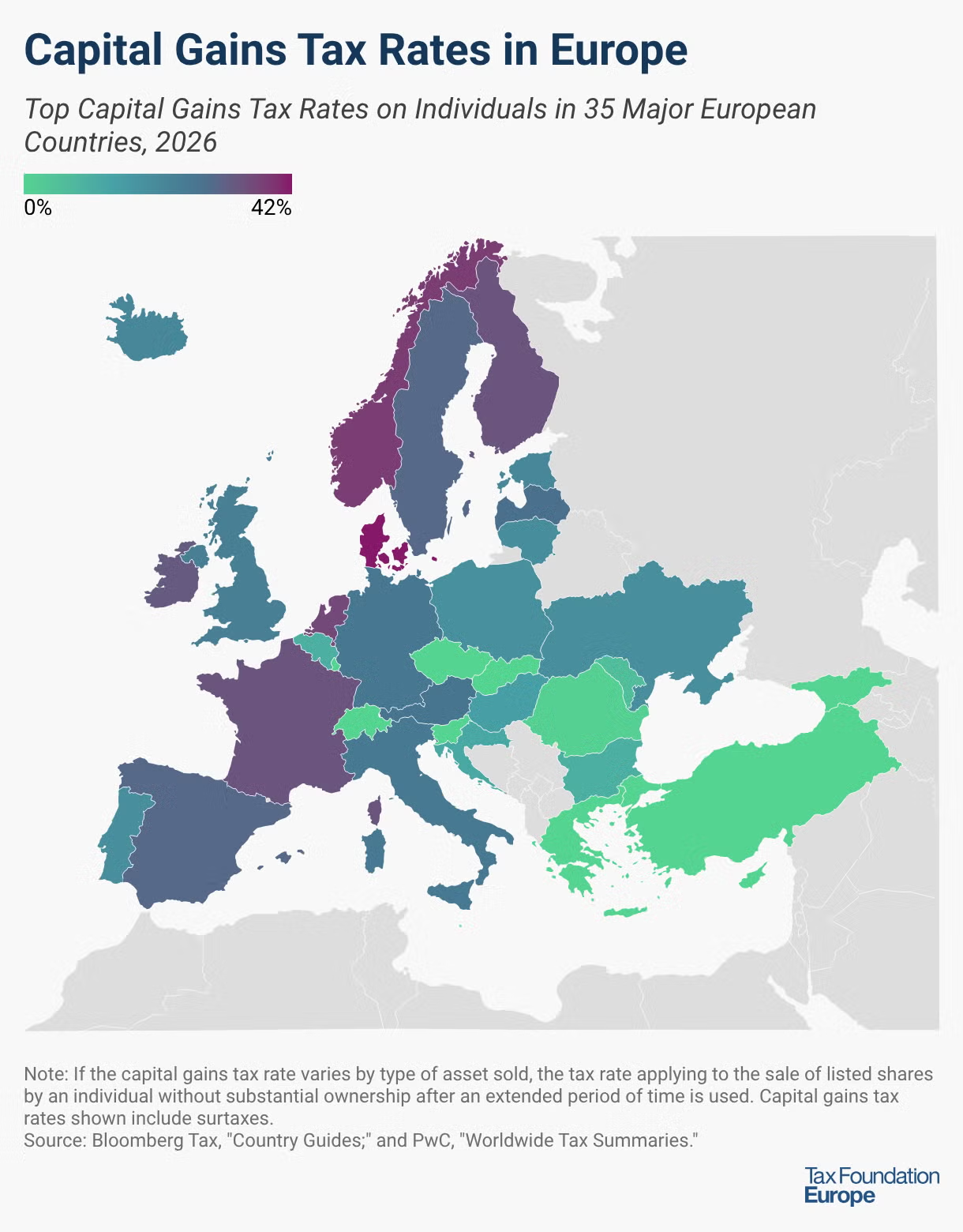

| Austria (AT) |

27.5% |

– |

| Belgium (BE) |

10.0% |

Capital gains from the sale of financial assets exceeding the annual exemption of 10,000 EUR will be taxed at 10%. Each year, 10% of the annual exemption can be carried forward for a maximum of five years. Capital gains from shareholdings of at least 20% are taxed at progressive rates up to 10%. Capital gains realized outside the normal management of someone’s private assets that are considered speculative gains remain subject to a 33% taxation. |

| Bulgaria (BG) |

10.0% |

Capital gains are subject to flat PIT rate at 10%. |

| Croatia (HR) |

12.0% |

– |

| Cyprus (CY) |

0.0% |

Shares listed on any recognised stock exchange are excluded from CGT. |

| Czech Republic (CZ) |

0.0% |

Capital gains included in PIT but exempt if shares of a joint stock company were held for at least three years (five years if limited liability company). |

| Denmark (DK) |

42.0% |

Capital income from shares up to DKK 79,400 is taxed at 27%. Share income in excess of this amount is taxed at 42%. |

| Estonia (EE) |

22.0% |

Capital gains are subject to PIT. From 20% in 2024 |

| Finland (FI) |

34.0% |

Capital gains are fully taxable and included in the taxable capital income subject to 30% tax rate up to taxable capital income of EUR 30,000 and 34% tax rate on the excess. |

| France (FR) |

34.0% |

Flat 30% tax on capital gains, plus 4% for high-income earners. |

| Germany (DE) |

26.4% |

Flat 25% tax on capital gains, plus a 5.5% solidarity surcharge. |

| Georgia (GE) |

0.0% |

Capital gains from shares held for more than two years is generally exempt from PIT. |

| Greece (GR) |

0.0% |

Capital gains only applies to the sale of shares at a 15% rate if an individual holds at least 0.5% of the share capital of the listed entity. |

| Hungary (HU) |

15.0% |

Capital gains are subject to flat PIT rate at 15%. |

| Iceland (IS) |

22.0% |

Exemption for capital income up to ISK 300,000 per year. |

| Ireland (IE) |

33.0% |

Annual gains of up to EUR 1,270 for an individual are exempt from CGT. |

| Italy (IT) |

26.0% |

– |

| Latvia (LV) |

28.5% |

Flat 25.5% on capital gains, plus 3% for high-income earners. |

| Lithuania (LT) |

20.0% |

Capital gains are subject to PIT, with a top rate of 20%. |

| Luxembourg (LU) |

0.0% |

Capital gains are tax-exempt if a movable asset (such as shares) was held for at least six months and is owned by a non-large shareholder. Taxed at progressive rates if held <6 months. aAdependency contribution of 1.4 percent is due for individuals subject to the Luxembourg social security system on the taxable part of the gains. |

| Malta (MT) |

0.0% |

Transfers of shares listed on recognized stock exchanges are usually exempt from PIT. |

| Moldova (MD) |

6.0% |

Capital gains are taxed at 50% of the PIT rate. |

| Netherlands (NL) |

36.0% |

Net asset value is taxed at a flat rate of 36% on a deemed annual return (the deemed annual return varies by the total value of assets owned) above an annual amount of EUR 59,357 per person. |

| Norway (NO) |

37.8% |

Capital gains are taxed at a 22% rate. A multiplier of 1.72 before taxation applies to gains from the sale of shares. |

| Poland (PL) |

19.0% |

– |

| Portugal (PT) |

19.6% |

PIT applies if the assets were held for less than one year. Otherwise, a flat capital gains tax rate of 28 percent from the sale of shares and other securities. Capital gains income is 10 percent tax-free for holding periods between 2 and 5 years, 20 percent for 5 to 8 years, and 30 percent after 8 years. |

| Romania (RO) |

1.0% |

Gains derived from the transfer of securities and from operations with derivative financial instruments through intermediaries are taxed at 3 percent for holding periods less than 356 days and at 1 percent thereafter. |

| Slovakia (SK) |

0.0% |

Shares are exempt from capital gains tax if they were held for more than one year and are not part of the business assets of the taxpayer. |

| Slovenia (SI) |

0.0% |

Capital gains rate of 0% if the asset was held for more than 15 years (rate up to 25% for periods less than 15 years). |

| Spain (ES) |

30.0% |

– |

| Sweden (SE) |

30.0% |

– |

| Switzerland (CH) |

0.0% |

Capital gains on movable assets such as shares are normally tax-exempt. |

| Turkey (TR) |

0.0% |

Shares that are traded on the Stock Exchange and that have been held for at least one year are tax-exempt (two years for joint stock companies). |

| Ukraine (UA) |

19.5% |

Capital gains are subject to PIT. |

| United Kingdom (GB) |

24.0% |

– |